Why MMC Has Struggled in the UK and How Affordable Housing and Robotics Can Change the Economics

Abstract

Despite sustained policy interest, Modern Methods of Construction (MMC) and off-site manufacturing (OSM) have achieved limited penetration in UK housing delivery. This paper argues that the primary constraint has not been technological capability but structural misalignment between manufacturing economics and the UK’s project-led housing market. Drawing on recent high-profile failures and contrasting examples of more successful application, it demonstrates that MMC performs best where demand is aggregated, typologies are repeatable, and delivery is programme-based. The analysis shows that affordable housing programmes provide the most credible context for MMC at scale, particularly when combined with factory-embedded robotics to reduce labour intensity and improve consistency. Conservative modelling indicates potential net savings of £14,000–£25,000 per dwelling where such conditions are met. The paper concludes that meaningful transformation in UK construction will depend less on further pilots and more on disciplined programme design, procurement reform, and strategic alignment between policy, industry structure, and technology adoption.

Why MMC Has Struggled in the UK and How Affordable Housing and Robotics Can Change the Economics

Over the past decade, Modern Methods of Construction (MMC) and off-site manufacturing (OSM) have been widely promoted as mechanisms to improve productivity, quality, and delivery speed in UK construction. In practice, however, their penetration into mainstream housing delivery has remained limited. This outcome is frequently attributed to technological immaturity or industry conservatism, yet the available evidence points to a more structural explanation: MMC has been deployed into a market environment that is fundamentally misaligned with manufacturing economics.

Evidence on the Structural Constraints Facing MMC in the UK

Recent high-profile failures in the UK MMC sector illustrate this misalignment clearly. Ilke Homes entered administration in 2023 after scaling a large, capital-intensive factory operation without securing a sufficiently stable, long-term pipeline of work. While the technical performance of its housing product was not the principal issue, the business model proved highly exposed to demand volatility and the absence of programme-level certainty.

A similar pattern occurred in the withdrawal of Legal & General Modular Homes, which halted new production and moved into a phased wind-down following sustained losses. The decision by a major institutional investor to exit modular housing was significant not only for the firm itself, but also for wider market confidence, reinforcing lender and insurer concerns regarding the risk profile of MMC manufacturing under prevailing UK delivery models.

More recently, TopHat ceased trading in late 2024 after several years of losses, while Lighthouse entered administration in 2024. These cases underline a consistent theme: scale and ambition alone are insufficient to sustain MMC businesses where demand remains fragmented, project-led, and sensitive to market cycles.

Taken together, these outcomes demonstrate that MMC has not failed because it delivers poor-quality buildings or lacks technical capability. Rather, it has struggled because factories have been required to absorb levels of market volatility that would normally be borne elsewhere in the development and construction value chain. In short, manufacturing has been introduced without the institutional and commercial structures required to support it.

Where MMC and robotics are being applied more successfully

Contrasting these failures with more stable applications of MMC highlights an important distinction. Where off-site manufacturing has been embedded within delivery models characterised by scale, repeatability, and long-term visibility of demand, performance has been markedly stronger.

Laing O’Rourke provides a notable example through its Explore Manufacturing facilities, which form part of a vertically integrated Design for Manufacture and Assembly (DfMA) strategy. The relative success of this approach is not attributable solely to off-site techniques, but to the alignment of manufacturing capability with large, multi-year infrastructure and public-sector programmes that support consistent utilisation and cumulative learning effects.

In volumetric construction, Tide Construction and Vision Modular Systems have demonstrated that modular approaches can be delivered at scale where typologies are tightly controlled and construction sequencing is predictable. While such projects are not without challenges, they illustrate that MMC can operate effectively when programme discipline is maintained.

A further example is Reds10, which has focused its off-site delivery on public-sector estates such as education, defence, and justice. These sectors are characterised by repeatable asset types, defined technical standards, and aggregated demand, making them more compatible with manufacturing-led delivery models.

Experience with robotics follows a similar pattern. In the UK, task-specific systems such as Hilti’s Jaibot, trialled by firms including Dalkia, have demonstrated measurable benefits in precision, safety, and productivity. However, these benefits are realised primarily where scope is tightly controlled. Dispersed, site-based deployment has generally struggled to achieve sufficient utilisation to justify investment. By contrast, robotics embedded within factory environments benefits from repeatability, high utilisation, and systematic quality control, materially strengthening the economics of MMC rather than attempting to substitute site labour directly.

Affordable housing as the critical enabling context

These contrasting outcomes point to the importance of delivery context. From a commercial perspective, affordable housing programmes represent the segment of the UK housing market most closely aligned with manufacturing principles. Such programmes typically involve aggregated demand across multiple sites, earlier design freeze, and acceptance of standardised solutions. Delivery objectives place greater emphasis on certainty, quality, and whole-life value than on sales absorption.

Consequently, affordable housing programmes supported by organisations such as Homes England provide a more credible foundation for off-site manufacturing at scale. They also create the conditions under which investment in factory automation and robotics can be justified, as utilisation risk is materially reduced and learning effects can be captured over time.

Quantitative implications for industry decision-makers

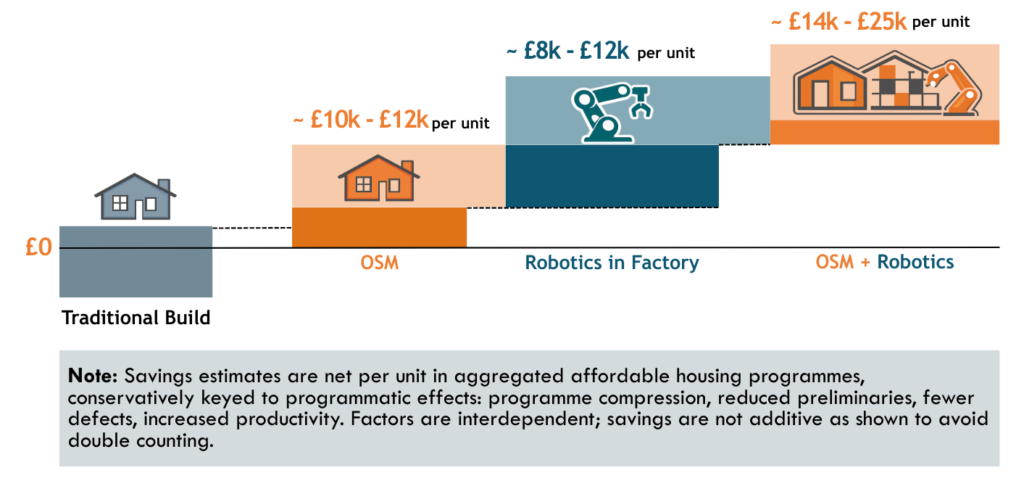

When assessed at programme rather than project level, the economic implications of MMC become clearer. Conservative modelling of affordable housing delivery indicates that off-site manufacturing alone can generate net savings in the order of £10,000–£18,000 per dwelling.[1] These savings are driven less by reductions in headline construction cost and more by programme compression, reduced preliminaries, and lower defect rates.

The integration of factory-embedded robotics further strengthens the business case. By reducing labour input on repeatable tasks and improving consistency and throughput, robotics can increase net savings to approximately £14,000–£25,000 per dwelling, with capital investment typically recoverable within two to three years where utilisation is sustained. The critical insight is that these returns are contingent on programme continuity; without it, the economics deteriorate rapidly.

[1] Base case costs are indicative and reflect a traditional, site-based affordable housing scheme in England, with an average construction cost of approximately £190,000 per dwelling. This estimate is informed by recent industry and public sector benchmarks, and is intended to represent an order-of-magnitude reference point for programme-level comparison rather than a project-specific cost estimate.

Exhibit 1: Comparative cost savings in housing construction: estimated net savings per unit in affordable housing programmes

Source: Misca Advisors analysis. Indicative savings ranges presented are derived from synthesis of UK public-sector guidance, industry studies, and programme-level modelling, based on a 300-unit development. Values are illustrative and intended to show order-of-magnitude impacts rather than project-specific guarantees.

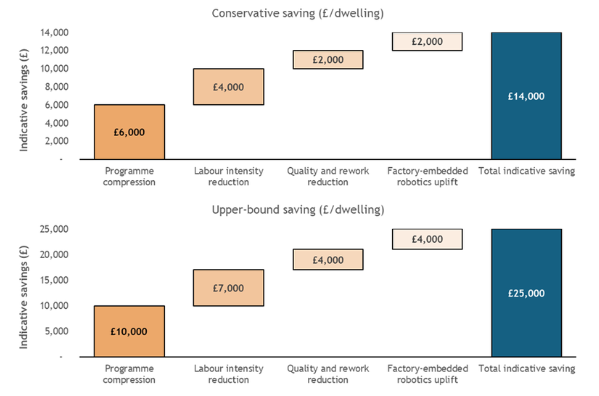

Exhibit 2: Composition of savings (MMC and robotics) – conservative vs upper bound scenarios

Note: Indicative, programme-level comparison of conservative and upper-bound savings versus a traditional build baseline. Not additive; illustrative only.

Source: Misca Advisors analysis

Strategic implications for industry

For developers, particularly those active in affordable housing and build-to-rent, the evidence points towards a shift from site-by-site optimisation to programme-based strategy. Contractors face a parallel transition, moving away from labour-intensive delivery models towards production management and integration capability. Building product manufacturers, meanwhile, have an opportunity to move up the value chain into systems, assemblies, and automated manufacture, provided that demand aggregation can be secured.

Lessons from UK MMC failures (and what to do differently)

Recent experience highlights a clear set of lessons. Factories were often built ahead of secured pipelines, project-by-project procurement models were applied to manufacturing systems, and speed benefits were not monetised in private sale housing. Robotics was frequently deployed without sufficient utilisation to justify investment.

By contrast, MMC performs best where demand is aggregated at programme level, typologies are standardised with early design freeze, factories are designed for high utilisation, and robotics is embedded in controlled environments. The key takeaway is that MMC and robotics are not silver bullets, but under the right commercial conditions they can materially reduce labour intensity, improve predictability, and strengthen margins.

Conclusion: from pilots to programmes

The UK construction sector does not suffer from a lack of innovation; it suffers from a lack of commercial alignment. The recent history of MMC shows that factories, automation, and robotics do not fail because they cannot deliver buildings, rather they fail when they are asked to operate in a fragmented, volatile, project-led market.

The evidence is now clear. MMC works when demand is aggregated, typologies are repeatable, and delivery is programme-led. Affordable housing is the segment where those conditions are most consistently present, and where the combination of off-site manufacturing and factory-embedded robotics can materially reduce labour intensity, improve predictability, and deliver measurable cost savings.

For industry, the shift required is strategic rather than technological: moving from site optimisation to portfolio and programme thinking, from labour substitution to production management, and from one-off pilots to scaled, investable platforms. For government and public clients, the prize is equally clear: the ability to tackle labour shortages and delivery constraints by reshaping how demand is structured, not by relying on an ever-scarcer workforce.

The next phase of transformation will not be driven by headline-grabbing prototypes. It will be driven by disciplined strategy, realistic economics, and sustained pipelines. That is where MMC and robotics can finally deliver on their promise, and where those who act early, with the right partners, will secure a durable advantage.

How Misca supports future construction strategies

Misca Advisors works with developers, contractors, and building product manufacturers as well as UK and other governments to navigate structural change in infrastructure, built environment and construction sectors. We support clients to assess where new ways of working are commercially viable, model realistic returns on investment, and design programme-based strategies aligned with market conditions.

Our work sits at the intersection of market and research intelligence, financial analysis, and policy-aware strategy, helping organisations reduce labour exposure, improve delivery certainty, and invest with confidence.

If you are exploring how new delivery models could shape your future pipeline, we’d be happy to talk.